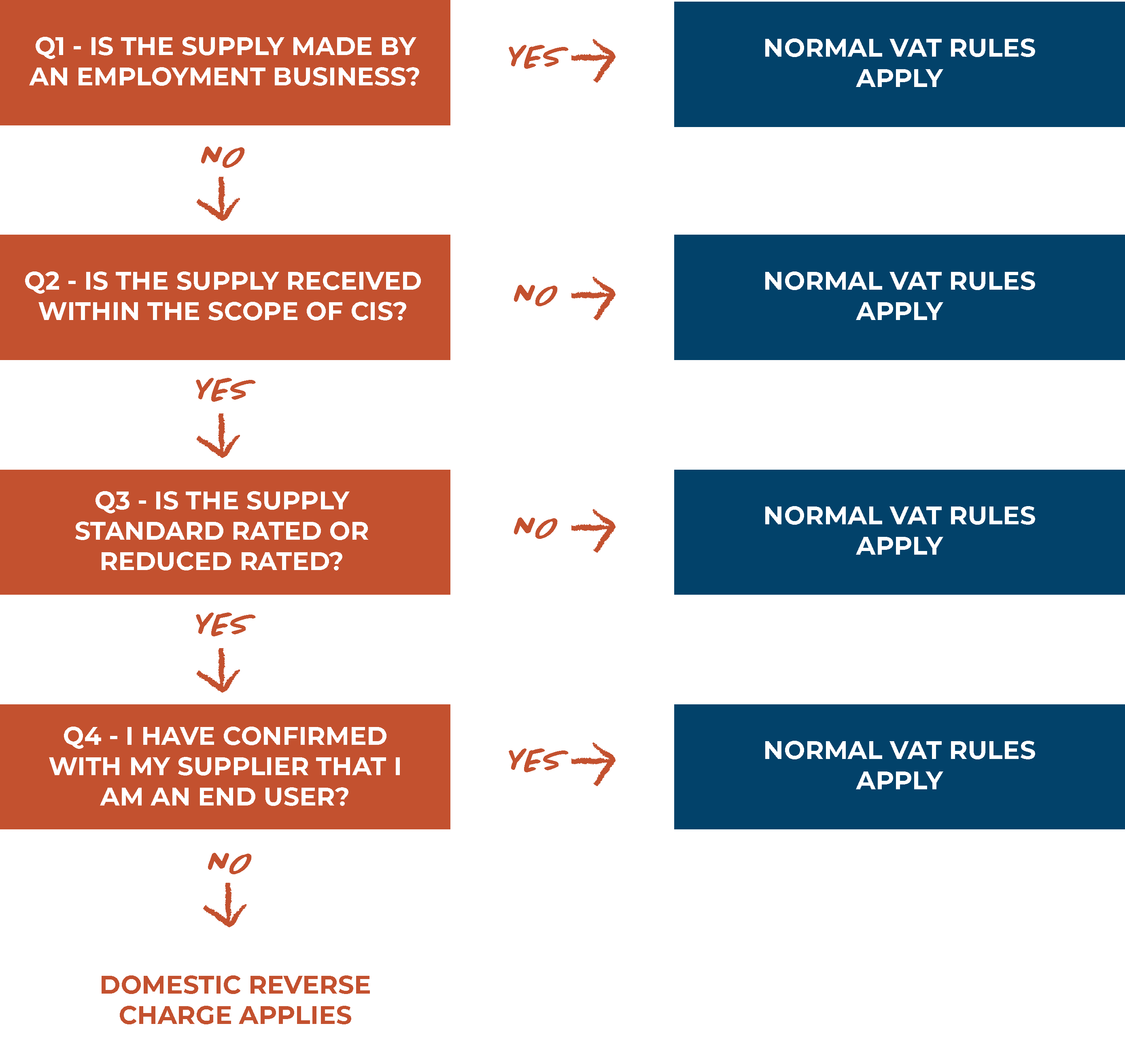

Reverse Charge Vat | If your business has two vat numbers, one in germany and another one in france, you may ask yourself why you charge vat in germany but not in france for two supplies that are similar in both countries. If more than 5% of contracts (in value or volume) are subject to the vat reverse charge, a contractor and subcontractor can agree to apply the charge to all contracts. You must use the reverse charge from 1 march 2021, if you're vat registered in the uk, supply building and construction industry services and: Reverse charge vat applies to the value of individual line items that are equal to or exceed the threshold amount. Reverse charge is a deviation from the general vat rules in which businesses usually charge vat on supplies and deduct vat on purchases. Both entries cancel each other out from a cash payment perspective and equal zero. Reverse charge vat from the perspective of customers and authorities when the reverse charge vat is applied, the buyer of your services declares both their purchase (called input vat) and their supplier's sale (called output vat) in their vat return. If your business buys services from outside the uk a rule called the 'reverse charge' applies. As the reverse charge work is 4.76% of the total invoice value (£500 / £10,500), you need to charge 20% vat on the whole invoice. Vat reverse charge in switzerland. The reverse charge mechanism is based solely on the tax status of the recipient of the goods or services since the vat is transferred to the buyer's country. When you buy goods or services from suppliers in other eu countries, the reverse charge moves the responsibility for the recording of a vat transaction from the seller to the buyer for that good or service. What is reverse charge vat? As the reverse charge work is 4.76% of the total invoice value (£500 / £10,500), you need to charge 20% vat on the whole invoice. It is also one of the reasons for which an invoice may not charge vat. If the vat reverse charge has already been used between two parties, both parties can agree to future services on a site being subject to the reverse charge. Convert the value of the services into sterling. However, the field of services, i.e. Under reverse charge mechanism (rcm), the supplier does not charge vat to the customer, the. Both entries cancel each other out from a cash payment perspective and equal zero. Reverse charge is a tax schema that moves the responsibility for the accounting and reporting of vat from the seller to the buyer of goods and/or services. The reverse charge mechanism under vat is mainly used for transactions from cross the border. (revenue.ie) eu reverse charge vat The reverse charge mechanism under vat is mainly used for transactions from cross the border. Vat reverse charge in switzerland. To find out when reverse charge vat should be used, check out the govt website : Vat reverse charge means that customers are able to charge themselves vat and pay it directly to hm revenue and customs (hmrc) rather than the supplier sending them an invoice at a later date, which in return stops suppliers from avoiding paying hmrc, also known as missing trader fraud. Reverse charge vat applies to the value of individual line items that are equal to or exceed the threshold amount. Reverse charge vat applies to the value of individual line items that are equal to or exceed the threshold amount. The reverse charge is the amount of vat you would have paid on that service if you had bought it in the uk. Reverse charged vat is used in some territories to collect tax on purchases from suppliers who are not subject to the tax authority's jurisdiction. Contrarily, the authorities will systematically. I've outlined a few scenarios based on the tax status of both the buyer and supplier below. In most cases both amounts will be the same and cancel each other out. You charge yourself the vat and then claim this back as input tax subject to the normal rules. The reverse charge was introduced in the eu to simplify the processing of transactions across borders, and for businesses that aren't vat registered in the country in which their business is based. The reverse charge mechanism under vat is mainly used for transactions from cross the border. It is also one of the reasons for which an invoice may not charge vat. Vat reverse charge in switzerland. In the purchase order sales tax group field, select the sales tax group that you created in the set up a sales tax group for reverse charge vat section. Calculate the amount of vat due and include this in. In case of a vat audit, they systematically refuse the refund of vat erroneously charged to the customer and apply fines and late interest if the reverse charge mechanism has not been applied. If your business has two vat numbers, one in germany and another one in france, you may ask yourself why you charge vat in germany but not in france for two supplies that are similar in both countries. You charge yourself the vat and then claim this back as input tax subject to the normal rules. However, the field of services, i.e. In a typical business, the supplier supplies goods to the customers and collect vat from the customers, which is later paid to the federal tax authority (fta). Reverse charge vat applies to the value of individual line items that are equal to or exceed the threshold amount. What is reverse charge vat? You must use the reverse charge from 1 march 2021, if you're vat registered in the uk, supply building and construction industry services and: To find out when reverse charge vat should be used, check out the govt website : This is where you act as if you're both the supplier and the customer. The reverse charge mechanism under vat is mainly used for transactions from cross the border. As the reverse charge work is 4.76% of the total invoice value (£500 / £10,500), you need to charge 20% vat on the whole invoice. However, in certain circumstances the recipient rather than the supplier, is obliged to account for the vat due. However, the field of services, i.e. Reverse charge vat from the perspective of customers and authorities when the reverse charge vat is applied, the buyer of your services declares both their purchase (called input vat) and their supplier's sale (called output vat) in their vat return. However, in certain circumstances, the recipient rather than the supplier is obliged to account for the vat due. This means that your client pays the vat and not you. Contrarily, the authorities will systematically.

Reverse Charge Vat: The reverse charge is the amount of vat you would have paid on that service if you had bought it in the uk.

0 komentar:

Posting Komentar